What is a Trump Account? The New Way to Save for Kids in 2026

America will turn 250 years old on July 4, 2026. Many will recall the joy and hope for a new future that our forefathers must have had as they signed the Declaration of Independence. As our citizens commemorate this milestone, the IRS will implement a new investment account that seeks to forge a strong path for the next generation of Americans: The Trump Account.

How Does a Trump Account Work?

The Trump Account (TA) is essentially a retirement account that can be funded for minor children, with features and tax benefits that are very similar to Traditional IRAs. The goal is to begin the savings and investment process early for them, so that young adults can jumpstart their financial journey.

Key Dates for Parents and Guardians

- Now: Parents, guardians, and grandparents can begin opening these accounts for eligible minors.

- July 4, 2026: This is the official date when you can begin making contributions.

The $1,000 “Seed” Money

To encourage long-term growth, the U.S. Treasury is providing a one-time benefit for newborns:

- Eligibility: Children born between January 1, 2025, and December 31, 2028.

- The Benefit: These accounts will receive a $1,000 contribution from the treasury as “seed” money.

To open a Trump Account, IRS form 4547 will need to be completed, or applicants can visit TrumpAccounts.gov and begin the application process there.

Not Sure Where to Start?

Begin your journey by meeting with an adviser to talk through your goals. We’ll help you find the right path forward — no obligation, just insight.

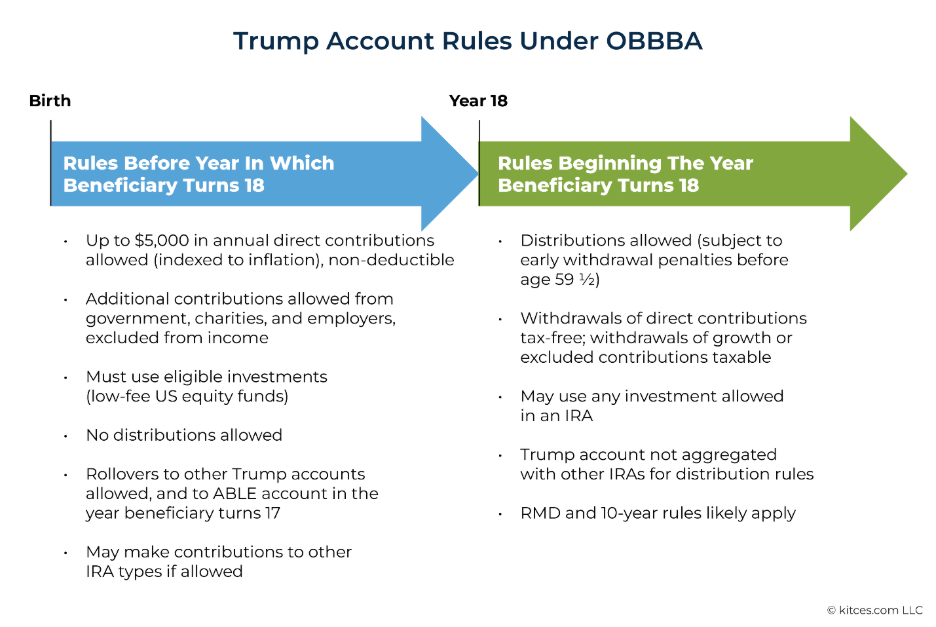

Contribution Rules & Limits

Beginning this year, the annual contribution limit is $5,000 but that limit is expected to grow with inflation in the future. These contributions can only be made until the child turns 18. Speaking of contributions, here are a few things to keep in mind:

- Anyone can contribute to a TA, including parents, relatives, friends, and even the child himself. These contributions are all post-tax and are not tax-deductible.

- If the child has a job in the future, his employer may contribute up to $2,500 to the TA. These are considered pre-tax contributions and will not count as income for the child.

- There are no income requirements to make contributions.

Withdrawal Rules: Staying the Course

In regard to withdrawals, there are some strict rules. When it comes time to take money out of the account, remember that:

- Withdrawals are not allowed before age 18.

- There is a 10% penalty if money is withdrawn before age 59.5.

- There are only a select few exceptions that will result in a penalty-free withdrawal pre-59.5, including costs for higher education, first-time home purchase, and disability.

- Growth on the investments will be taxed at ordinary income tax rates.

Should you open a Trump Account?

If you have a have an eligible child in your life or expect to have one in the next few years, it will likely be worthwhile to open one of these accounts. Even if you don’t plan on contributing more money in the future, the $1,000 contribution from the Treasury will certainly be a benefit in the future. Starting early for children will be extremely valuable to their future.

There are several other planning questions that you may want to discuss with your financial advisor, such as the differences between a TA and a Custodial Account or 529, Kiddie Taxes, and Roth conversion options in the future. This will be a great conversation if you have gifting goals to the next generation and will help you determine if a TA is right for you. As the nation looks ahead to its next 250 years, the current financial environment is creating encouraging opportunities for future Americans.