Most seniors rely on Medicare to provide their health insurance coverage. In 2015, 16.3 percent of all people in the United States were covered by Medicare1. That number continues to grow as our population ages.

Medicare does not cover everything. Medicare is divided into three parts: Part A, Part B, and Part D. In general terms, Part A covers hospital related expenses. Part B covers doctor’s services and outpatient medical services such as — laboratory tests, X‑rays, and therapy. Part D is the prescription drug benefit. Part A has a coinsurance payment set at a dollar amount you pay for each day in the hospital within a certain range of days over 60. Part B also has a coinsurance that is typically 20% of the Medicare-approved amount for most doctor services, outpatient therapy and durable medical equipment. Part D may have a deductible depending on the plan chosen by the insured. The maximum annual deductible is $405 in 2018.

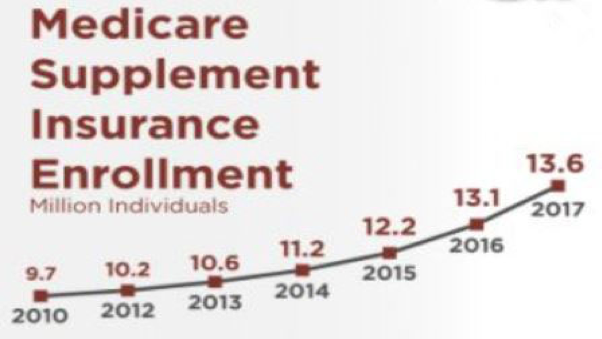

For 2018, the Part A deductible is $1,340 per year, and the Part B deductible is $183. Additionally, there are unlimited costs in Part A after you’ve used up your lifetime reserve days, plus the insured is responsible for 20% coinsurance for Part B services. Many people buy a Medicare supplement policy (Medigap) to protect themselves from the risk of an injury or illness costs exceeding their Medicare coverage.

Source: American Association for Medicare Supplemental Insurance

Medicare Supplement Plans

There are 10 standardized Medicare Supplement Plans, including Plans A, B, C, D, F, G, K, L, M, and N as well as one high-deductible plan. Plan F has been by far the most popular even though it is the most expensive plan. More than half of all consumers select Plan F over all the others combined because it is the most comprehensive plan that eliminates almost all retiree healthcare cost surprises by absorbing virtually all deductibles, co-payments, and coinsurance with any service providers that accept Medicare patients.

Source: American Association for Medicare Supplemental Insurance

As part of the Medicare Access and CHIP Reauthorization Act of 2015, Medigap Plan F and Plan C options will no longer be available to new enrollees after 2020.

Plan F and Plan C are considered Cadillac plans, and this change is a shift under Medicare to ensure that consumers are paying something out-of-pocket for their healthcare.

Medicare Supplement Plan G

Many consumers may change to Plan G. Plan G is nearly identical to Plan F except it requires a $183 per year deductible that must first be satisfied (which avoids the Cadillac plan label). The average Plan G is nearly $30 per month less than Plan F. Consumers that would reach the deductible would save nearly double on the lower premium costs. Rates differ by state and insurance company, but the national average for Plan F premiums is $185.96 a month, compared with $155.70 for Plan G2.

Anyone already in Plan F at the end of 2019 will be able to keep the plan. However, if you are in Medicare now and buy a Medicare Advantage plan or another Medigap insurance plan, switching after January 1, 2020 may be difficult. Most states allow insurance companies to screen for conditions ranging from diabetes to heart attacks and cancer. On that basis, you could be turned away from Plan F or face high premiums.

There is some concern in the industry that monthly premiums for these plans could change once insurance companies see the effects of the 2020 changes. Plan G rates could increase because Medicare rules require plans to accept enrollees regardless of health conditions. Plan F rates could also increase because new 65-year-olds, who are generally healthier, will no longer be able to buy the plan. It will all depend as insurance companies examine the claims of participants in both Plan F and Plan G.

Rick’s Tips:

- Medicare insurance has gaps in its coverage that can be insured by purchasing a supplemental insurance policy.

- There are currently 10 standardized Medicare Supplement Plans, including Plans A, B, C, D, F, G, K, L, M, and N plus one high-deductible plan.

- Plan F is the most popular, but it will no longer be available to new enrollees after December 31, 2019.

1 Source: Statista.com

2 Medicare Supplement Plans are changing: What you need to know. Reuters by Gail Mark Javis. September 18, 2018