HELOC stands for home equity line of credit. Like a mortgage, it’s a loan made against the equity in your home. HELOCs have two phases, 1) the draw period, and 2) the repayment period.

Draw Period

During the draw period, most loans offer the ability to pay interest-only for a set number of years. The interest rate will fluctuate based on an agreed upon benchmark interest rate, for most loans that’s the Federal Reserve’s Prime Rate. The rate for a HELOC might be expressed something like Prime Rate + 0.50% (currently 4.75% + 0.50% = 5.25%).

During the draw period you’ll only be charged interest on the outstanding balance, so if you pay off the balance, you won’t have any interest charges due. Additionally, if you pay off a portion of your balance, your required payment goes down. This is unlike a traditional mortgage, where if you pay additional amounts towards the principal, the monthly payment required remains the same.

Repayment Period

During the repayment period, the loan payments will increase sharply because you’ll begin paying back principal and interest. Each bank will have different lengths of draw periods and repayment periods, so it’s important to understand the terms of the loan before taking it out. Many banks will have a 15- or 20-year repayment period that begins after a 5- or 10-year draw period.

HELOCs and Conventional Mortgage Amortization Tables

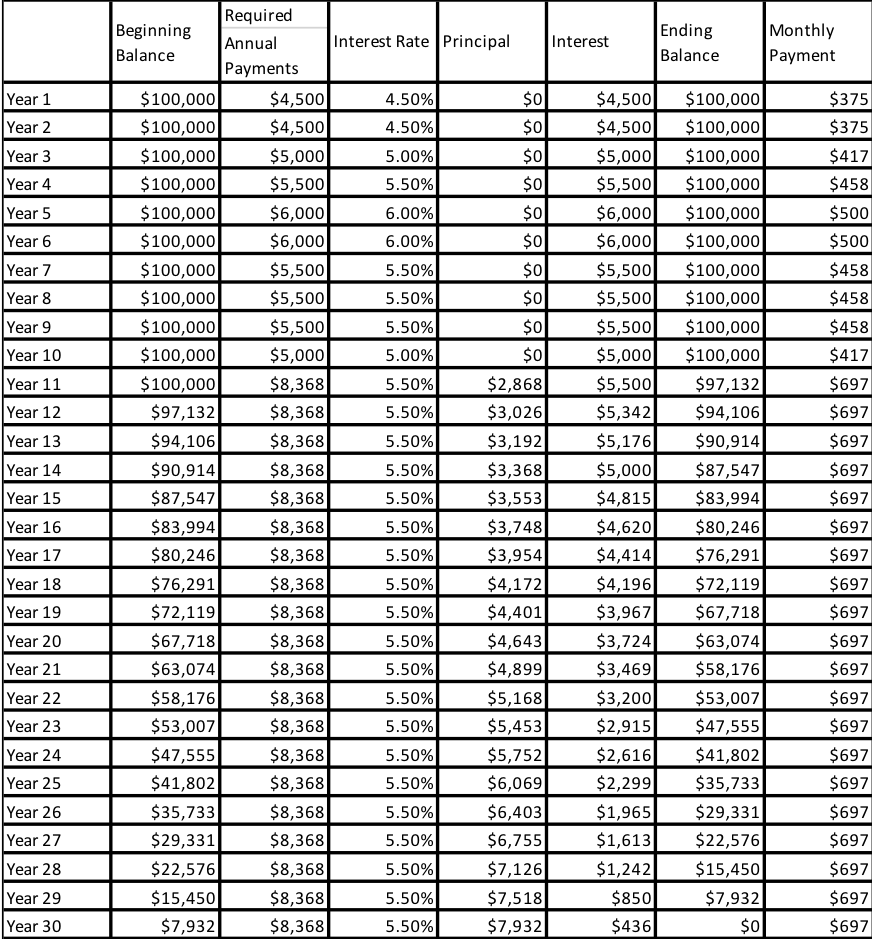

To further illustrate the differences between HELOCs and conventional mortgages, I’ve included two hypothetical amortization tables below. I’m assuming that this HELOC offers a 10-year draw period with a 20-year repayment period. With the HELOC, you can see that the interest rate fluctuates during the draw period and then becomes a fixed rate once the 20-year repayment period begins. At that point, the payment increases substantially because the payments will begin to include both principal and interest.

To contrast that against a conventional 30-year fixed rate mortgage, you can see that the rate is constant and that each payment includes part principal and part interest over the life of the loan.

HELOC Table

Fixed Rate Mortgage Table

Advantages Over Conventional Mortgages

There are several reasons that HELOCs can have significant advantages over mortgages but the largest two are flexibility and cost. With a HELOC, you’re only required to pay interest on any balance you have outstanding. You can draw $100,000 today, pay off $100,000 tomorrow, and then draw $100,000 against it the day after that. Let’s say your car suddenly broke down and you didn’t want to take any additional withdrawals from your IRA in the current tax year. You could borrow $30,000, pay interest-only during the current year, and then pay off the full balance in January when the next tax year begins. I recently worked with a client that did something similar, and while it cost her about $1,000 of interest, pushing the withdrawal to the next year saved her about $6,000 of taxes.

Also, unlike a traditional mortgage where there are significant closing costs in the form of title insurance, origination fees, notary charges, deed recording fees, most HELOCs don’t cost anything to establish.

There are costs that are incurred, but in most cases the bank will pick up the costs. Some banks will charge a fee if the HELOC is completely closed out within a specific period of time. Closing the line out would mean you’ve eliminated your ability to draw against it. You can always pay the loan off without actually closing it out.

In some cases, the interest on a HELOC may be tax deductible. Under the new tax law, in order for interest to be considered tax deductible, the loan needs to be used for “acquisition debt.” An example of acquisition debt would be used to purchase or to “substantially improve” your home. If the proceeds were used for buying a car or paying off a credit card, the interest would not be tax deductible. It’s worth pointing out though that under the new tax law, the vast majority of people will no longer be itemizing their deductions. While HELOC interest may be deductible if you’re itemizing, if you’re not itemizing you should probably just evaluate the loan based solely on its own merits rather than planning to have the interest costs lower your tax bill.

One other advantage is that many banks will offer promotional interest rates for the beginning of the loan. Their hope is obviously that you’ll keep your balance in place after the promotional period expires but you’re likely under no obligation to do so.

Disadvantages of HELOCs

The primary disadvantage of a HELOC is that it’s a variable interest rate, so if rates go up your payment will too. Many HELOCs will have a cap on how high the rate can go, but it’s important to discuss this with your lender.

One other potential disadvantage is that if you don’t have enough equity in your home, this may not be an option for you. Most of the banks are willing to give you a line large enough so that the total balance of the HELOC and any mortgage debt you have doesn’t exceed 80% of the value of your home (this is called your loan to value ratio). For example, if your house is worth $300,000, the most that your mortgage plus your HELOC can add up to is $240,000. Some banks may allow you to do a higher loan to value ratio but will generally charge you more interest because it’s considered a riskier loan.

From a borrower’s perspective, it’s important to remember that having a relatively small interest-only payment obligation has a tendency to mask how much you actually owe. If you owe $10,000 and your interest rate is 5%, your monthly payment is only about $42. You should carefully evaluate what you’re using the HELOC for and not allow it to become a crutch to enable increased spending.

There’s also a surprising amount of variation in terms between different banks, so it’s very important to understand the differences of your particular lender’s terms. Here are the questions that I think are important to ask:

- How long is the draw period?

- How long is the repayment period?

- What is the interest rate?

- Are you offering any promotional interest rates and if so how long is it in place for?

- Are there any discounts offered for having my other banking relationships with you?

- During the draw period, am I required to pay interest only, or is there a minimum dollar amount I’ll need to pay if my interest is less than it (for example, the greater of $50 or the current interest due)?

- What loan to value (LTV) ratio will you lend up to in order to qualify for your best interest rate?

- Are there any fees I’d be responsible for to start the loan?

- Are there any fees I’d be responsible for if I close out the loan before a certain period of time?

HELOCs can be an extremely powerful tool when used properly. There is certainly potential for misuse as we saw during the 2008 financial crisis. But for many responsible borrowers, they can be an empowering and invaluable resource.