You are probably aware of the IRA penalty for taking money out of an IRA or Roth IRA too early. Distributions prior to age 59½ are subject to tax and a 10% penalty (see exceptions). You may also be aware of the penalty for taking distributions too late. Required minimum distributions from an IRA must begin by April 1 of the year following the year you turn 72. Failure to take the minimum distribution will result in a 50% penalty of the required distribution not taken. Were you aware there is also a penalty for contributing too much to your IRA?

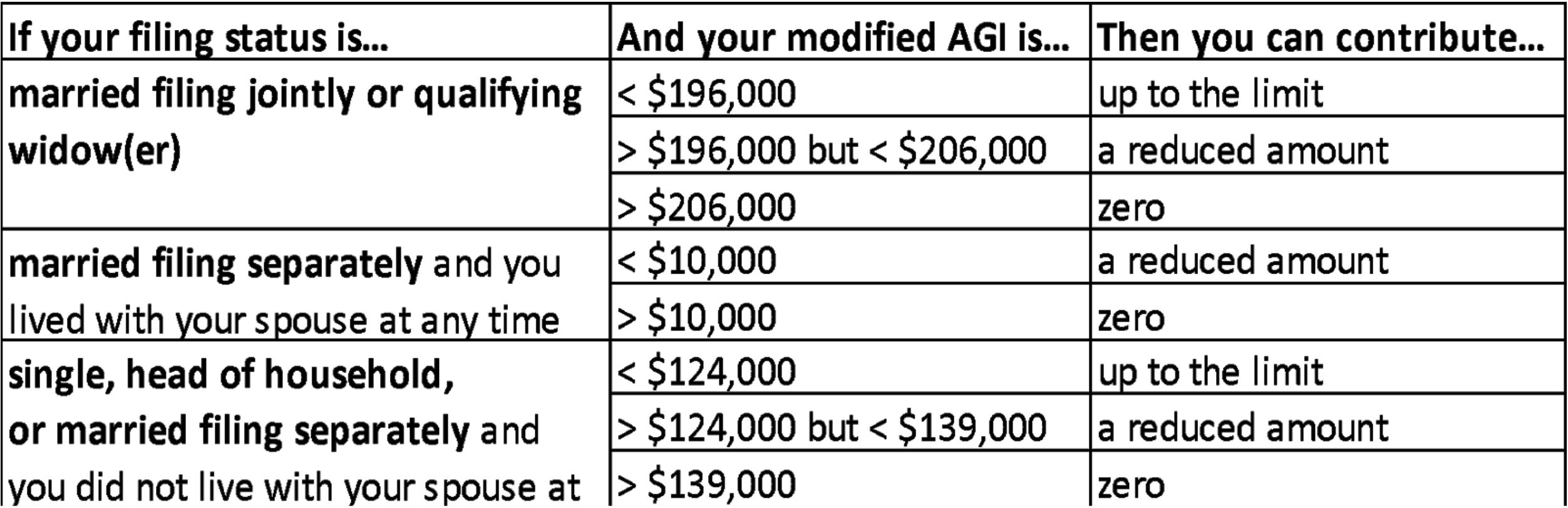

The contribution limit to a traditional IRA or Roth IRA for 2020 is $6,000 (or $7,000 if you’re 50 or older). You must have earned income of these amounts or file jointly with someone who does. Contributing more than this amount in a tax year will result in an excess contribution. For Roth IRAs, there is also an income limit. Taxpayers need to be aware of and stay within these statutory contribution limits to avoid penalties. See table below:

October 15 is the deadline for withdrawing excess contributions for the prior year to avoid a 6% tax penalty. You are required to pay the 6% tax each year that the excess amount remains in your traditional IRA or Roth IRA. Therefore, if you made an excess contribution to an IRA in 2020 and failed to withdraw the excess until 2021, you will owe 6% on the amount for each year.

Excess contributions can also be caused by:

Missed 60-Day Rollover Rule – If you take a lump-sum distribution from your employer plan or another IRA, you have 60 days to complete the rollover to another IRA. After 60 days, you must treat the distribution as taxable income unless you receive a waiver, or extension, of the 60-day period from the IRS. You may also be subject to the 10% premature distribution penalty if you are not 59½ when the distribution occurred.

Once-Per-Year Rollover Rule – Once you successfully complete an IRA rollover within the 60-day limit, you cannot make any additional rollovers within a 12 month period. The once-a-year rule only applies to IRA-to-IRA rollovers. It does not apply to eligible rollover distributions from an employer plan such as a 401(k), 403(b) or 457(b). You may roll over more than one distribution from a qualified plan to another qualified plan or IRA account within a year.

Required Minimum Distributions (RMDs) – RMDs cannot be rolled over to an IRA to avoid paying tax on the distribution. You can still do an IRA rollover but not with the RMD amount. You also cannot convert the RMD to a Roth IRA. Be sure to distribute the RMD completely before processing an IRA rollover or Roth conversion with any remaining balance in your IRA.

Traditional IRA and Roth IRA Contributions – You are allowed to contribute to both a traditional IRA and Roth IRA in the same tax year provided the combined contributions do not exceed the annual limit. It could make sense to split contributions when a deductible contribution will put the taxpayer in a lower tax bracket. This is especially true for taxpayers who move from the 22% tax bracket back into the 12% tax bracket.

IRA Contributions after Age 72 - Following the passage of the SECURE Act in December 2019, workers over age 72 can still contribute to an IRA provided they meet the earned income requirement. However, that same worker must also begin taking required minimum distributions. It may seem silly to put money into the same account that has mandatory withdrawal requirements. Making the contribution to a Roth IRA instead may be more beneficial over the long term.

Excess IRA contributions can be corrected by removing the excess amount and any applicable earnings on the excess from the IRA by the taxpayer’s filing deadline (generally April 15). The excess can still be removed without penalty by October 15 as taxpayers receive an automatic six-month extension on the deadline for removing the excess amount. After the second deadline, the excess accrues a 6% penalty for every year it remains in the IRA. You need to act quickly once an error is discovered to stop the penalty meter from running.

Rick’s Insights

- The excess contribution penalty of 6% can be avoided if the excess is removed by the taxpayer’s filing deadline including extensions.

- Missing the 60-day rollover window can result in the entire distribution becoming taxable and subject to the early withdrawal penalty.

- The Required Minimum Distribution amount is never eligible for rollover or conversion to a Roth IRA.